Distribution Is the Last Step. Most Brands Treat It Like the First.

What the RNDC collapse proved about account list ownership, performance standards, and why the legal structure of your distribution agreement is a sales infrastructure decision

TL;DR

The build sequence is clear: account relationships first, velocity proof second, market intelligence third, distribution as fulfillment fourth. Each phase creates the leverage the next phase requires.

The compliance infrastructure embedded in a traditional distributor’s 30–35% margin costs a brand doing $500,000 in annual revenue roughly $150,000–$175,000 per year. The equivalent technology stack costs $6,000–$33,000. That gap funds owned sales capacity.

RNDC — once the second-largest U.S. spirits distributor — is dissolving. Brands that had built owned account relationships and alternative channel infrastructure transitioned with minimal disruption. Brands that hadn’t are waiting months for remittances and scrambling for new partners. That is not a hypothetical argument for owned infrastructure. It is the empirical one.

Part 1 diagnosed the problem. Part 2 profiled what the alternative looks like. This article answers: how do you actually build it?

The sequence is not complex. The discipline to follow it is. And as of May 2026, the argument for building it has moved from structural to urgent. RNDC, once the second-largest U.S. wine and spirits distributor, is in the process of complete dissolution. Its 38-state footprint is being absorbed by at least five separate acquirers — Reyes Beverage Group (11 states, closing end of May 2026), Martignetti Companies, Columbia Distributing, Breakthru, and Quality Brands, all in letter-of-intent stage. Hundreds of small producers are waiting months for remittances. Brands without owned account relationships or alternative channel infrastructure are scrambling for new partners under compressed timelines.

The brands that transitioned cleanly share a profile: they knew their own accounts, they had direct buyer relationships, and they had distribution options that weren’t contingent on one entity. That profile is what this article describes how to build.

The Four Components and Why Sequence Matters

Account relationships are the foundation — documented connections with specific buyers that belong to the brand. These are your negotiating currency with every distributor, chain buyer, and investor. Nosotros Tequila, which had originally built California presence through Park Street before transitioning to RNDC, re-activated that infrastructure during the 90-day RNDC exit window. Their Chief Revenue Officer described the result directly: “The fact that we own this conversation and are placing orders, our team is having hands-on conversations with every buying contact in the state.” Since transitioning, Nosotros saw a significant boost in business both on- and off-premise. The owned relationship was the difference between a disruption and an opportunity.

Velocity proof is what account relationships produce over time. LTO Consulting’s benchmark: 10 accounts with a minimum 2 cases per month reorder rate, at 80%+ reorder frequency, before approaching traditional distribution. That is roughly 30 cases per month — essentially the average small producer’s entire annual output, concentrated in a single proof-of-concept market. It sounds like a lot. It is achievable in one city before you approach a distributor for that market.

Market intelligence is what most brands outsource entirely to distributor-provided reports, which are structurally incentivized to be incomplete. Distributors have no obligation to share account-level sell-through data. Brands that own their intelligence — through direct account relationships, platform analytics, and independent tracking tools — know which accounts are performing, which are dormant, and whether their distributor is selling or warehousing.

Brand equity is what survives a distributor relationship ending. Account relationships that belong to the brand, consumers who seek out the product at retail, on-premise social proof. The 92% retail synergy finding from the 2024 Sovos/Harris Poll study captures the mechanism: 92% of craft spirits enthusiasts likely to buy DTC say they would subsequently look for that brand at retail. Consumer relationships built direct don’t stay direct — they feed wholesale demand.

Why sequence matters: A brand entering a distribution conversation with documented velocity data and named account relationships negotiates terms. A brand asking a distributor to create that demand accepts terms. The RNDC collapse made this visible at scale: brands with owned infrastructure transitioned. Brands without it scrambled.

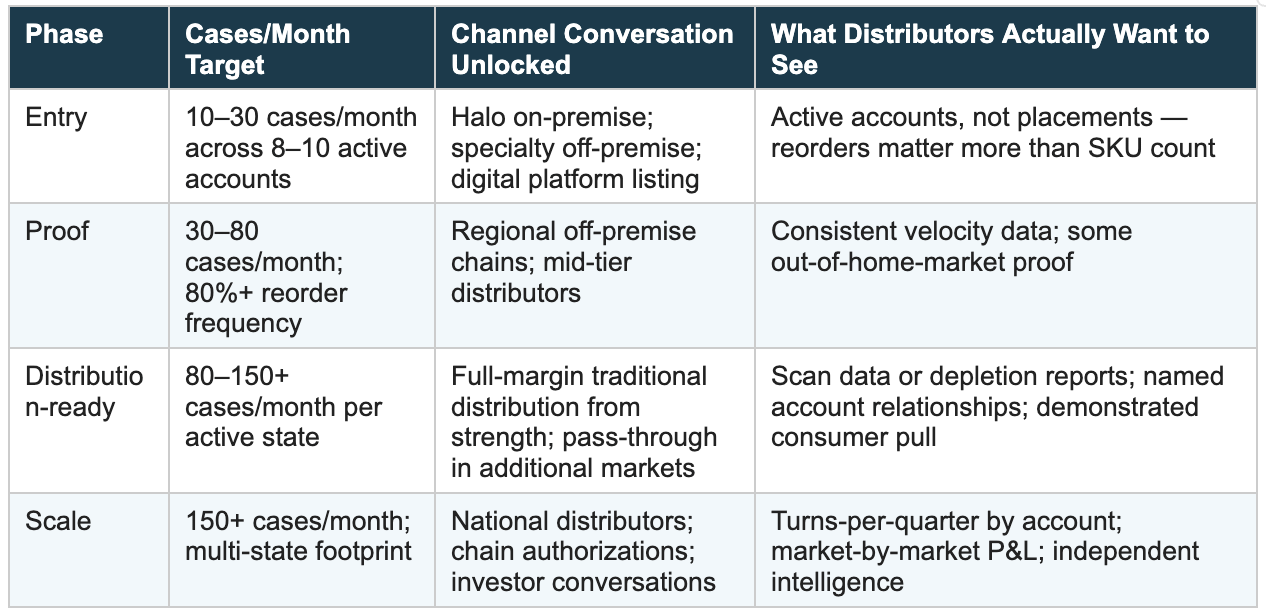

Velocity Benchmarks: What Distribution-Ready Actually Means in 2026

The ACSA 2025 data covers full-year 2024. Volume: 12.7 million nine-liter cases, down 6.1% — the second consecutive annual decline. Active craft distilleries: 2,282, down 25.6% in 12 months from 3,069. Average small producer output: 531 cases per year. The category is contracting. The brands that survive will be the ones with owned demand, not the ones waiting for distribution to create it.

What distribution-readiness looks like at each scale is not formally published, but emerges consistently from practitioner guidance:

Velocity Benchmarks by Phase

The velocity proof required for each channel conversation differs. Entering without it is entering without leverage.

Sources: ACSA 2025 Craft Spirits Data Project (Oct 2025); LTO Consulting distributor survey guidance (2024); Park Street/ACSA conference practitioner panel (2019). Case-per-month thresholds are practitioner estimates; no published industry standard exists.

A note on the entry-phase math: 10 accounts at 2 to 3 cases per month is 20 to 30 cases per month from that proof-of-concept cluster. That is more than some brands generate across their entire operation. The point is the principle, not the number. A concentrated, documented, reordering account base in one market tells a distributor more than 100 placements that never reordered.

The context matters in 2026: with RNDC dissolving and successor distributors (Reyes, Martignetti, Columbia) absorbing portfolios they did not build, the minimum viable velocity story for getting meaningful attention from a new distributor relationship is higher, not lower. These entities are optimizing inherited portfolios. A brand arriving with documented velocity proof is demonstrably different from one asking the new distributor to build demand from scratch.

For brands currently in RNDC markets: Run this diagnostic before the close date: how many of your placements are actively reordering versus registered but dormant? The successor distributor will rationalize the inherited portfolio. Brands with documented velocity proof have leverage in that conversation. Brands without it are at the bottom of a prioritization list that doesn’t know they exist.

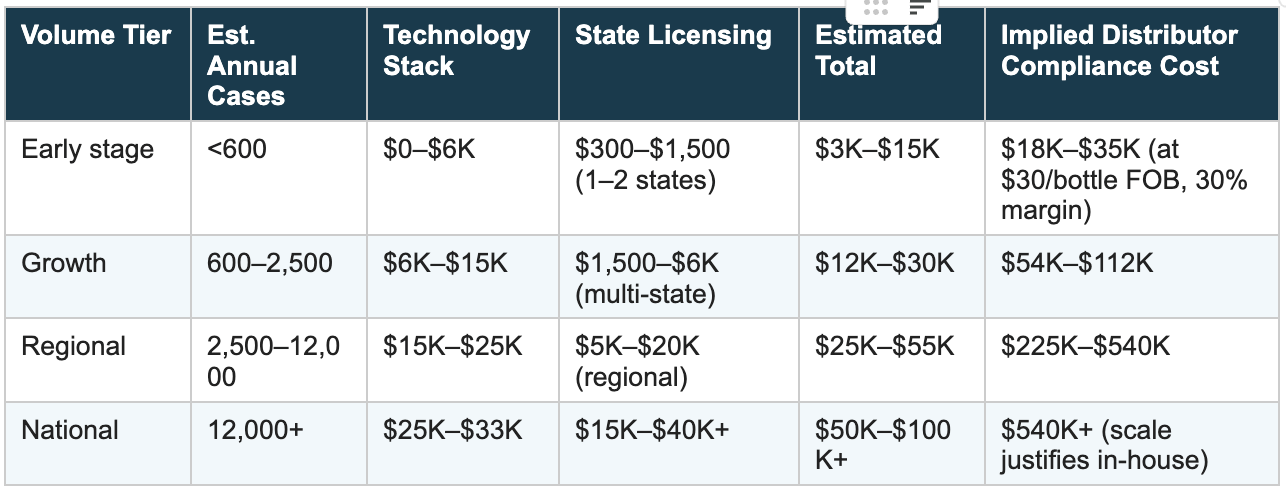

The Compliance Cost Equation — And What’s Changed

The distributor margin already includes the cost of compliance — you are paying for it whether you see the line item or not. For a brand doing $500,000 in annual revenue, the compliance function embedded in a 30 to 35% distributor margin costs $150,000 to $175,000 per year. The equivalent technology-enabled compliance stack costs $6,000 to $33,000 per year. That is a margin recapture of $117,000 to $160,000 annually on the same revenue base.

One meaningful update: TTB processing times have improved dramatically. The article’s prior guidance cited 12 to 14 month average timelines for Distilled Spirits Plant permits. TTB’s current published medians run 45 to 81 days (March/April 2026 data), with label approvals at 6 days and formula approvals at 7 to 15 days. The compliance bottleneck has shifted from federal permit approval to state-level brand registration and label approval processes, which vary widely by state and are not tracked by TTB. The strategic implication: the regulatory delay that justified long lead times at the federal level has compressed. State compliance remains the variable that demands automation.

The DTC channel now has one significant new addition: California AB 1246, signed October 2025, effective January 1, 2026, allows qualifying out-of-state distillers (producing no more than 150,000 gallons annually) to ship up to 2.25 liters per consumer per day directly to California residents. Permit cost: $30 annually plus $125 initial application. The program is a one-year pilot, expiring December 31, 2026. California is the largest spirits consumer market in the U.S. — this is the most significant DTC expansion in years, and its temporary status makes early activation a priority for any brand that qualifies.

Compliance Infrastructure Cost by Volume Tier

Component costs vary significantly by volume and geographic footprint. Assembled from platform documentation and practitioner estimates.

Sources: Maguey Exchange industry analysis (Dec 2025); LibDib/Thirstie platform documentation; TTB fee schedules; TTB Processing Times updated April 22, 2026. Implied distributor compliance cost derived from standard margin structure at $30/bottle FOB.

On DTC and California specifically: The California pilot (through Dec 31, 2026) expires unless extended. Any brand qualifying under the 150,000-gallon threshold should activate the $155 permit immediately. The program’s temporary status is not a reason to wait — it is a reason to move. Building a California DTC consumer database during the pilot period creates durable value regardless of what happens to the program. The DTC permissive state count now stands at 10 states plus D.C. The gap versus wine (48 states) remains, but California changes the DTC calculus materially.

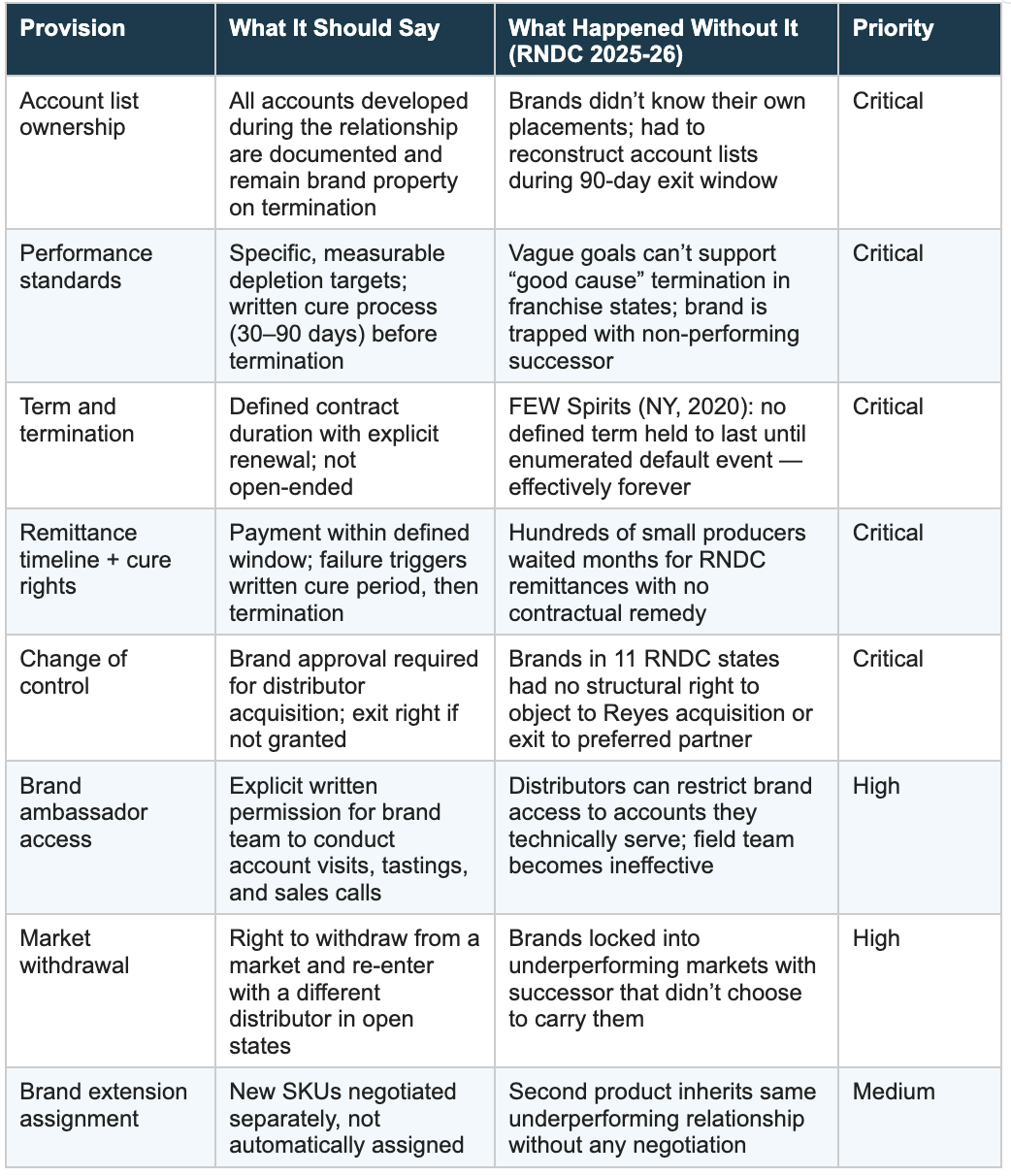

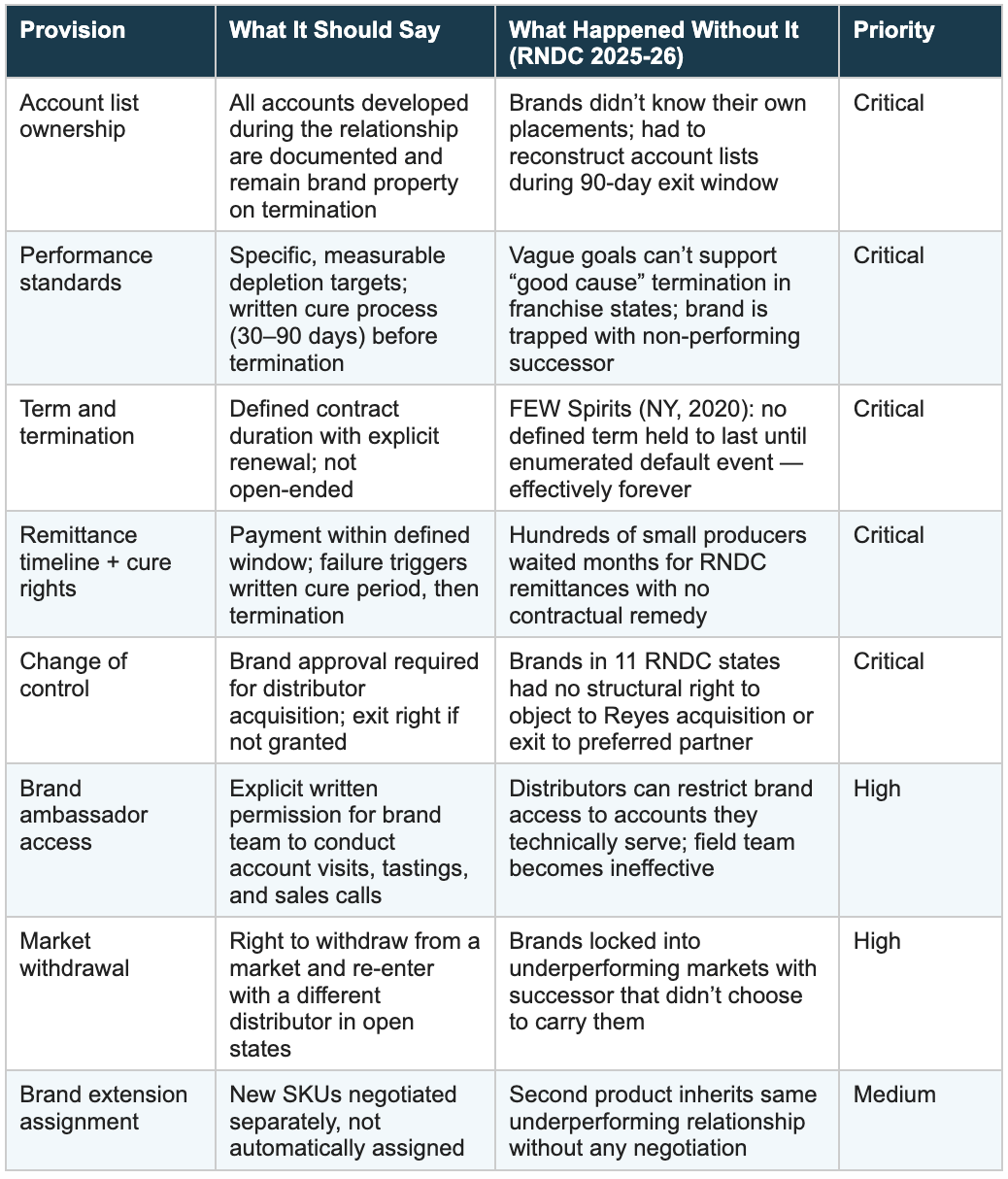

What to Negotiate Before You Sign Anything — And What 2025 Proved

Most craft brands sign distribution agreements drafted by the distributor’s counsel, reviewed by nobody, and accepted because the milestone felt important. The RNDC collapse turned that abstract risk into documented outcomes. Here is what happened to brands across two profiles:

Brands without account list documentation didn’t know their own placements when RNDC exited — they had to reconstruct account lists from memory and distributor reports that were months out of date. Brands without remittance cure provisions waited months for payment with no contractual remedy. Brands without change-of-control termination rights had no structural ability to exit to a distributor of their choice. Brands with owned infrastructure and documented accounts — like Nosotros Tequila — activated alternative channels during the 90-day exit window and grew through the transition.

The Jägermeister/Missouri franchise law case, resolved in May 2025, added legal clarity on one critical point: the 8th Circuit confirmed that without a written trademark license from manufacturer to distributor, spirits franchise protections do not attach — even for decades-long oral arrangements. This is the single most actionable franchise law development in years. It confirms that the structure of your written agreement — specifically the absence of a trademark license grant to the distributor — is a structural defense against franchise claims in 8th Circuit jurisdiction.

Distribution Agreement: What to Negotiate and What Most Brands Miss

Every item below is standard in well-represented brand agreements. Most brands signing their first deal have none of them. The RNDC collapse is the evidence.

Sources: McDermott Will & Emery distribution agreement guidance (2023); FEW Spirits v. distributor (NY, 2020); Park Street RNDC Transition Analysis (Apr 30, 2026); Jagermeister/Major Brands 8th Circuit ruling (Nov 2024) and dismissal (May 2025).

The franchise law advantage for spirits brands remains intact and unchanged. Beer franchise protection exists in nearly every state. Spirits franchise protection exists in roughly half — and even where it exists, it is typically narrower. The Missouri Jägermeister ruling confirms: the absence of a written trademark license is a structural defense. Spirits brands in open states that enter agreements with undefined terms, no performance standards, and no account list ownership clauses are accepting the worst possible legal position before the first case is sold.

For brands in RNDC markets right now (May 2026): Three immediate actions before the close date: (1) Request written confirmation of continued representation from the successor entity. (2) Document every current placement — account name, address, reorder history — as your account list, in writing. (3) Exercise any change-of-control termination rights in your existing agreement if available, and negotiate transition terms explicitly. The 90-day window is the moment of maximum leverage. Once the acquisition closes, the successor owns the relationship. You own it only if your contract says you do.

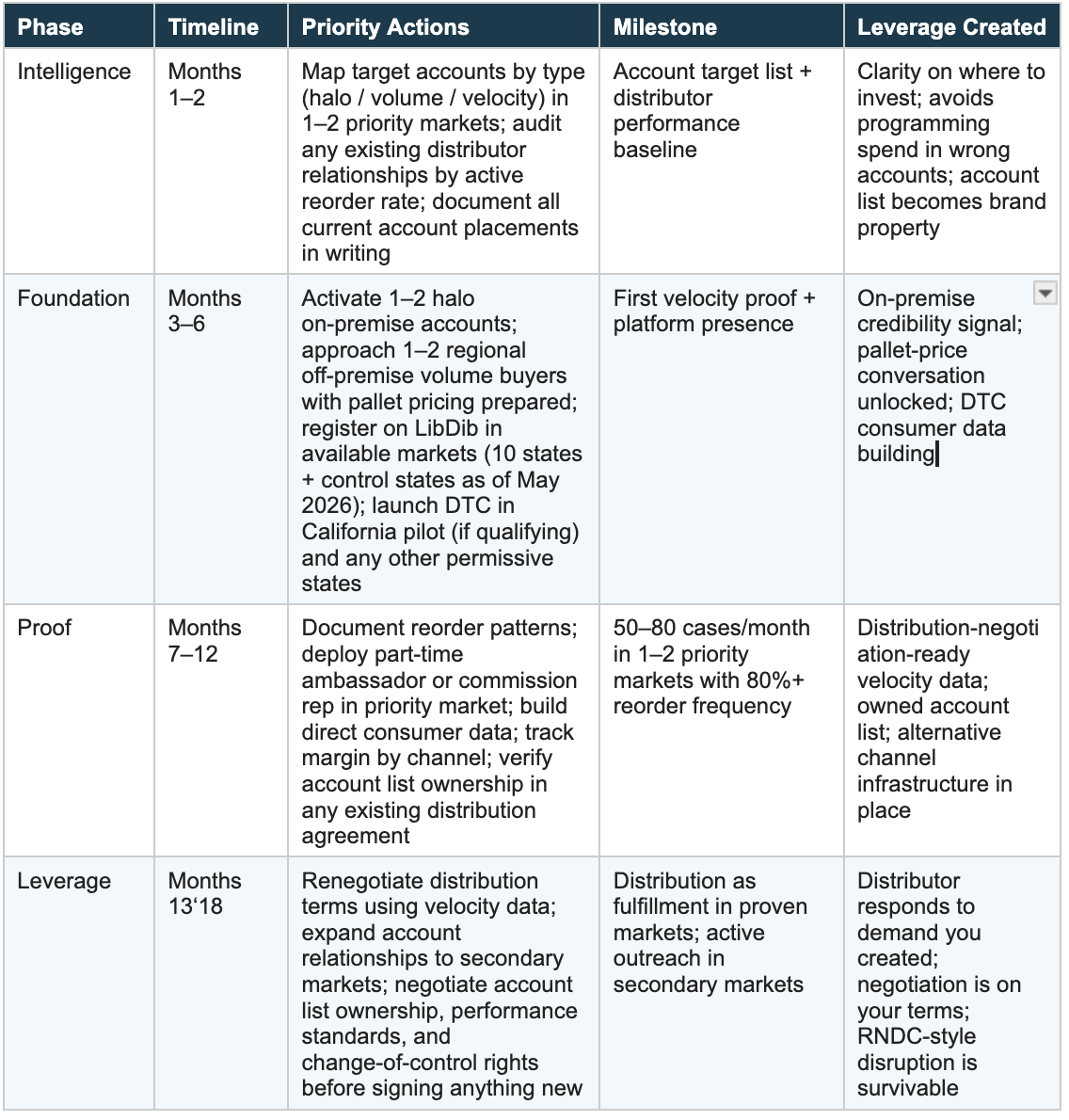

The 18-Month Build Sequence — Updated for 2026 Market Conditions

The timelines below incorporate the updated TTB processing environment (DSP permits now running 45 to 81 days median, down from the 12 to 14 months previously described) and the restructured digital platform landscape. The sequence is designed to be executed with limited capital — each phase is funded by the margin recapture from the previous one.

The most material platform change: the LibDib/RNDC On Demand network that previously offered 18-state digital access no longer exists at that scale. As of May 14, 2026, LibDib operates as a licensed distributor in California, Colorado, Connecticut, D.C., Florida, Illinois, Maryland, New Jersey, New York, and Wisconsin, plus Pennsylvania and Utah as control states. The On Demand program continues in one market (Tennessee, via Best Brands partnership). Brands planning a platform-first market entry strategy should now approach it state by state rather than assuming an 18-state network.

The 18-Month Sales Infrastructure Build Sequence (Updated May 2026)

Sequence is the key variable. Brands that execute these phases out of order spend capital without building leverage.

Sources: McDermott Will & Emery distribution agreement guidance (2023); FEW Spirits v. distributor (NY, 2020); Park Street RNDC Transition Analysis (Apr 30, 2026); Jagermeister/Major Brands 8th Circuit ruling (Nov 2024) and dismissal (May 2025).

The franchise law advantage for spirits brands remains intact and unchanged. Beer franchise protection exists in nearly every state. Spirits franchise protection exists in roughly half — and even where it exists, it is typically narrower. The Missouri Jägermeister ruling confirms: the absence of a written trademark license is a structural defense. Spirits brands in open states that enter agreements with undefined terms, no performance standards, and no account list ownership clauses are accepting the worst possible legal position before the first case is sold.

For brands in RNDC markets right now (May 2026): Three immediate actions before the close date: (1) Request written confirmation of continued representation from the successor entity. (2) Document every current placement — account name, address, reorder history — as your account list, in writing. (3) Exercise any change-of-control termination rights in your existing agreement if available, and negotiate transition terms explicitly. The 90-day window is the moment of maximum leverage. Once the acquisition closes, the successor owns the relationship. You own it only if your contract says you do.

The 18-Month Build Sequence — Updated for 2026 Market Conditions

The timelines below incorporate the updated TTB processing environment (DSP permits now running 45 to 81 days median, down from the 12 to 14 months previously described) and the restructured digital platform landscape. The sequence is designed to be executed with limited capital — each phase is funded by the margin recapture from the previous one.

The most material platform change: the LibDib/RNDC On Demand network that previously offered 18-state digital access no longer exists at that scale. As of May 14, 2026, LibDib operates as a licensed distributor in California, Colorado, Connecticut, D.C., Florida, Illinois, Maryland, New Jersey, New York, and Wisconsin, plus Pennsylvania and Utah as control states. The On Demand program continues in one market (Tennessee, via Best Brands partnership). Brands planning a platform-first market entry strategy should now approach it state by state rather than assuming an 18-state network.

The 18-Month Sales Infrastructure Build Sequence (Updated May 2026)

Sequence is the key variable. Brands that execute these phases out of order spend capital without building leverage.

Sources: ACSA/Park Street practitioner framework; TTB Processing Times (updated April 22, 2026); LTO Consulting velocity guidance (2024); LibDib platform status (May 14, 2026); McDermott Will & Emery distribution agreement guidance (2023).

Casa Dragones built along this sequence before the terminology existed. Co-founded in 2009 by Bertha González Nieves — the first woman certified as Maestra Tequilera — the brand spent a decade building category credibility through experiential marketing, halo placements, and direct consumer relationships before pursuing broad distribution. By 2019 it operated in 33 U.S. markets. Only then did it sign a national alignment with Southern Glazer’s, expanding to 44 markets from a position of demonstrated demand. The Nosotros Tequila transition in 2026 adds a more recent and more specific proof point: building owned infrastructure is not just a growth strategy. It is what allows a brand to survive a distributor collapse and emerge stronger.

On the agave spirits tariff situation (as of May 2026): Tequila and mezcal brands face live uncertainty on U.S. import tariffs. The USMCA exemption established in March 2025 covers virtually all commercially produced agave spirits meeting rules of origin. However, some tariff tracking sources cite IEEPA authority as potentially overriding USMCA treatment for Mexican spirits. The situation is legally contested and practically unresolved. Brands should: (1) consult Park Street’s live tariff tracker and DISCUS’s tariff timeline for current status, (2) verify USMCA compliance documentation with their importer, and (3) not assume a specific rate is stable. Do not state a current rate without a date qualifier — this is a live situation.

Own Your Market Intelligence

Without independent market intelligence tools, a craft brand’s only view into its own performance is what the distributor chooses to share. In RNDC markets from 2025 through early 2026, that meant many brands discovered the full extent of their distribution problem only when remittances stopped arriving and reps stopped returning calls. Owning your market intelligence means you know before the distributor tells you.

The market intelligence landscape divides into enterprise-tier tools and brand-accessible tools. SipSource (WSWA) — the only verified source of distributor depletion data — is priced for distributors and major suppliers. NielsenIQ and SPINS operate at six-figure enterprise contract pricing, generally inaccessible below 12,000 cases annually.

The most accessible platform designed explicitly for alcohol brands at varying scale is Overproof: AI-driven account prospecting, field sales activity tracking, depletion data by account and region, and reporting that is independent of distributor cooperation. The platform does not require the distributor to share data — which is the gap it fills. LibDib, in its current 10-state plus control state footprint, provides a foundational intelligence layer for brands using digital distribution: visibility into which accounts order, at what frequency, and in what quantities. For brands in the Foundation and Proof phases, that is enough to make evidence-based decisions about where to concentrate field investment.

The intelligence question to answer for every market: Not ‘are we in distribution?’ but ‘how many of our placements are actively reordering, and at what frequency?’ A brand that can answer that question with its own data — not from a distributor report — knows where it stands. That knowledge is what makes the distributor renegotiation conversation possible. It is also what made the difference between the brands that navigated the RNDC transition and the ones that didn’t.

The Long Fuse, and What It Burns Toward

The spirits industry has always rewarded a particular kind of patience. Not the passive patience of waiting for a distributor to prioritize you, but the active patience of building account relationships, reorder data, and brand equity while the distributor’s reps are occupied elsewhere. By the time the distribution conversation happens, the active-patience brand has something to negotiate with.

The RNDC collapse made that patience visible in a way no industry argument could. The brands that survived it intact were not the ones with the best products or the strongest distributor relationships. They were the ones that knew their own accounts, had their own conversations, and had infrastructure that didn’t depend on one entity’s continued operation. Hundreds of small producers who didn’t have that are waiting for remittances that are months overdue from a company that is dissolving.

There is a moment that industry veterans describe with a specific kind of satisfaction: the first time a distributor comes to them. The call where the distributor says, “we’ve been noticing your brand in markets we thought we controlled. Can we talk?” That call is what the sequence in this article builds toward. The brands getting it right now didn’t wait for distribution to build their sales engine. They built it themselves and let distribution become the fulfillment layer it was always supposed to be.

What’s the one thing you’d do differently in your first distribution agreement knowing what 2025 produced? I’d genuinely like to know.

Rob! Excellent insights. Thank you.